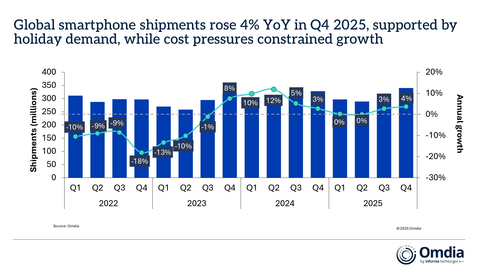

According to Omdia’s latest research, the global smartphone market grew 4% year on year in Q4 2025, supported by seasonal demand and improved inventory discipline, even as rising component costs began to weigh on a few vendors. Growth was concentrated among leading vendors, including Apple and Samsung, across key regions. Apple led the smartphone market in 4Q25 with a 25% market share, delivering a record fourth quarter driven by strong demand for the iPhone 17 series. Apple also ranked as the world’s largest smartphone vendor for the third consecutive year, finishing marginally ahead of Samsung.

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20260114416098/en/

Global smartphone shipments rose 4% YoY in Q4 2025, supported by holiday demand, while cost pressures constrained growth

In 4Q25, Samsung followed in second with 18% share, driven by strong momentum in the sub-$300 segment, particularly for the Galaxy A17 4G and 5G models. Xiaomi retained its third place for both 4Q and full year 2025, despite its share declining to 11% in Q4 amid hurdles to volume in some of its key markets. vivo captured 8% share, delivering another strong quarter predominantly driven by its leadership in India. OPPO re-entered the global top five as it returned to growth in 4Q, marking a positive turnaround ahead of its integration of realme into its business from January 2026.

For the full year 2025, global shipments grew 2% year-on-year to 1.25 billion units, reflecting a stable but uneven recovery year in which a weaker 1H25 was followed by a stronger second half, defined by booming emerging economies and positive reception of flagship launches. However, rising memory costs and shortages have started to impact the market and constrain the broader volume upside in 4Q25. Mounting cost pressures toward year-end point to a stronger focus on pricing discipline, profitability and operational efficiency heading into 2026.

“Apple recorded its highest-ever fourth-quarter shipment volumes in 4Q25,” said Sanyam Chaurasia, Principal Analyst at Omdia. “The performance was driven by solid demand for the iPhone 17 series alongside continued traction from older-generation models during the holiday season. The base iPhone 17 exceeded expectations following storage upgrades at unchanged pricing, while Pro models gained momentum as Apple ramped up production through the quarter. Meanwhile, the iPhone Air acted as a portfolio showcase, with its slim form factor enhancing retail marketing and reinforcing the premium appeal of the Pro lineup.

“DRAM supply tightness has added considerable supply-side pressures to the smartphone industry, and is expected to be a key defining factor in 2026, said Runar Bjørhovde, Senior Analyst at Omdia. “Amid restricted DRAM supply of both LPDDR4 and LPDDR5, the battle to secure supply and limit cost increases is intense amongst all vendors. All vendors are utilizing mitigating tactics, for example, by emphasising long-term partnerships, utilizing scale to secure capacity, and focusing on their supplier base. The situation is particularly critical for vendors with heavier exposure to entry-level smartphones, which are highly price elastic and where memory and storage costs make up a higher share of the bill-of-materials.”

“Rising cost pressures are reshaping how smartphone vendors approach 2026,” added Sanyam Chaurasia, Principal Analyst at Omdia. “Higher semiconductor costs, alongside a slowing refresh cycle, are expected to weigh on shipment momentum. In response, vendors are tightening configurations, aligning launch strategies closer with component availability and using channel-led levers such as services, trade-ins and ecosystem bundling to support higher price points. The push toward greater scale and supply-side leverage is already becoming evident, exemplified by realme moving under OPPO’s umbrella, reflecting early signs of consolidation as vendors seek greater scale to manage rising costs to maintain competitiveness in the decade’s second half.”

Worldwide smartphone market share split

|

|||

Vendor |

4Q25 market share |

4Q24 market share |

|

Apple |

25% |

23% |

|

Samsung |

18% |

16% |

|

Xiaomi |

11% |

13% |

|

vivo |

8% |

8% |

|

OPPO |

8% |

7% |

|

Others |

30% |

32% |

|

|

|

|

|

Note: Preliminary estimates are subject to change on final release

|

|||

ABOUT OMDIA

Omdia, part of Informa TechTarget, Inc. (Nasdaq: TTGT), is a technology research and advisory group. Our deep knowledge of tech markets grounded in real conversations with industry leaders and hundreds of thousands of data points, make our market intelligence our clients’ strategic advantage. From R&D to ROI, we identify the greatest opportunities and move the industry forward.

View source version on businesswire.com: https://www.businesswire.com/news/home/20260114416098/en/

© Business Wire, Inc.

Advertencia :

Este comunicado de prensa no es un documento producido por AFP. AFP no será responsable de su contenido. Para cualquier pregunta relacionada, por favor póngase en contacto con las personas/entidades mencionadas en el comunicado de prensa.